What is counselling insurance?

Insurance for counsellors is rarely a single product. Usually, one or more insurance products will be required depending on the specific needs of your counselling business.

Given the nature of your work as a counsellor, professional indemnity should always be central to your insurance mix. If you meet clients face-to-face, you may need to add public liability. Portable electronics might be required if you depend on expensive computer equipment for your work.

Why do counsellors need insurance?

Counsellors are exposed daily to clients who don't feel themselves and need someone else's guidance to get emotionally and mentally better. This responsibility does carry legal obligations and risks if things go wrong.

Financial claims from unhappy clients

Sometimes, counselling advice can lead to adverse outcomes. If your advice goes badly wrong, a dissatisfied client can demand compensation.

Accusation of overstepping the boundaries

As a counsellor, you conduct a lot of one-on-one sessions. If you say something and it’s taken out of context or considered discriminatory, you may face legal action.

Client injury on your premises

If you see clients face-to-face at your premises, there are risks of trips or falls during sessions with you.

Contract or professional body compliance

Specific insurance will be required if you are an independent counsellor or aspiring to become a member of an association or a professional body. Professional indemnity insurance will be essential, and public liability might also be required.

Damage to your work equipment

Suppose you use a laptop or computer to store your clients' files or conduct video sessions; if this gets lost, damaged or stolen, this will cause significant work disruption and financial burden.

Professional indemnity insurance for counsellors

Most self-employed counsellors should have professional indemnity insurance.

Professional indemnity is a legal cover that defends you if you face a legal claim due to your work. It provides legal advice and representation and pays compensation if due.

What does professional indemnity insurance for counsellors cover?

Professional indemnity protects counsellors from claims or accusations of wrongdoing from their professional advice or work product.

Cover includes:

- Failing your duty of care

- Making a mistake

- Acting negligently

- Giving the wrong advice or recommendation

For example:

- A client claims your professional advice caused them harm

- You failed to give the correct direction to a client when you should have

- You shared a client's confidential information with an unauthorised party

- You acted in a discriminatory manner

- You caused offence

Choosing a counselling professional indemnity limit that’s right

Selecting a reasonable professional indemnity limit for your counselling work is not always obvious; consider the following:

- If you're part of a counselling organisation, they usually specify the professional indemnity limit they require—some need as high as £2,000,000.

- If you're an independent counsellor, consider your level of qualification, experience, history of disputes with your clients, and the type of therapy you provide—the more complex your work, the higher the limit you might need.

- Think about what downside there might be if your advice goes wrong. How much might it cost to rectify?

- Some insurance providers offer as little as £50,000 of cover, which might be tempting as the price will be low. However, with the rising cost of legal services, ask yourself if this amount will go far enough to cover solicitors' fees and possible compensation.

Does professional indemnity insurance cover my counselling activities worldwide?

Your professional indemnity policy's ‘territory or geographical limits’ and ‘jurisdiction’ sections specify if your counsellor insurance will respond when working in different countries.

Territory or geographical limits:

The territory or geographical limit specifies where you can virtually or physically deliver your services. For example: “Worldwide.”

Jurisdictional limit:

The jurisdictional limit specifies which legal jurisdictions your policy will defend you if you are sued. For example: “Worldwide excluding US and Canada.”

Contract governance:

Any contracts or agreements you enter into with your clients should specify the ‘governing law’ for that contract, which is the jurisdiction in which parties can seek legal remedy for breach of contract.

Avoid entering contracts not governed by your local jurisdiction and/or excluded by your counselling professional indemnity insurance.

If you work with US and Canadian clients, you can reduce your risk by not entering contracts governed by US and Canadian laws.

Switching your professional indemnity insurance

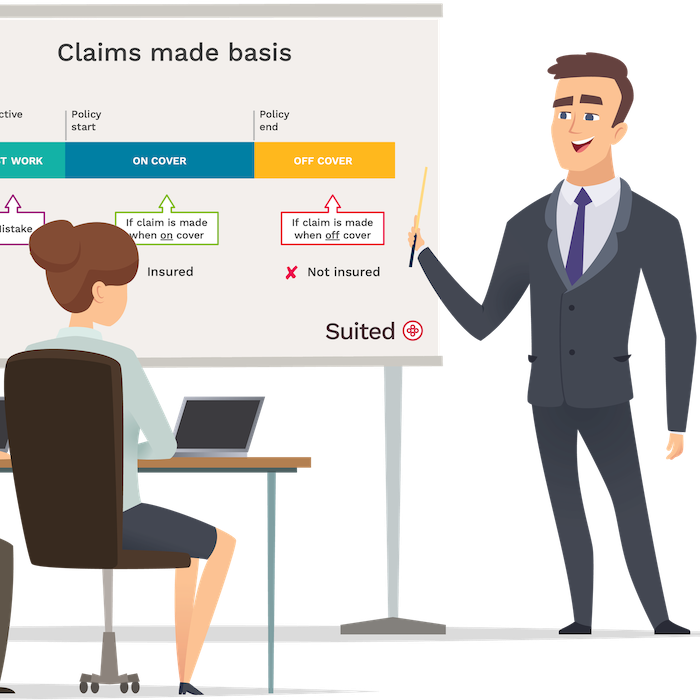

Typically, in the UK, if you cancel a professional indemnity policy, you can no longer claim against it.

Therefore, if you switch your counsellor insurance provider, be sure your new policy covers your past work; this is called “retroactive cover”.

Should I keep professional indemnity insurance if I pause my counselling activities?

It’s wise to keep your professional indemnity if you’re taking a break or retiring from counselling. Claims against professional misconduct can surface months or years after you delivered the work.

Remember: If you cancel your policy, your insurance coverage will end, including coverage for any previous work.

How long you keep your cover in place is up to you. Consider the type of counselling you did and the likelihood that a client might bring a claim against you.

Public liability insurance for counsellors

Public liability insurance is also becoming commonly needed by independent counsellors.

Most counsellors meet clients at their homes, at their clients’ homes or the office. Face-to-face meetings can expose counsellors to liability if clients trip or fall.

Public liability takes care of instances where your client may have had an accident and is now asking for compensation. Alternatively, you managed to damage a client’s property (e.g. knock over an expensive vase) and asked to pay for it.

What does counsellor public liability insurance cover?

Public liability provides legal defence and covers a possible payout if you're found liable for property damage or causing an injury.

Cover includes:

- accidental injury or death

- accidental property damage

For example:

- A client visits you at your home and is injured in a slip or fall

- You see a client at home and ruin their new carpet by knocking over a cup of coffee

Other insurance counsellors buy

As a counsellor, your other insurance coverage needs may differ based on your situation. Do you rely on expensive computer equipment for your work? What if you were unable to work due to illness? Would you be able to handle unpaid invoices? Do you have employees?

Commercial legal expenses insurance

Commercial legal expenses insurance is designed to support professionals such as counsellors with a range of legal and tax-related matters that fall outside the scope of professional indemnity or public liability insurance.

This type of cover can provide access to advice, representation, and practical support when facing legal or regulatory challenges in the course of running your business.

Typical areas covered include:

- Legal and accountancy matters relating to your business

- Defence against criminal prosecution

- Compliance and regulatory investigations

- Pursuit of unpaid invoices (typically over a set threshold)

Examples of when it might be useful:

- You're flagged for an IR35 or other tax investigation by HMRC

- You need to chase a client for a large unpaid invoice

- You’re facing a compliance issue and require expert legal guidance

Commercial legal expenses insurance often comes with access to helplines and resources to help navigate these situations more effectively.

Portable electronics insurance

As an independent counsellor, your business operations probably heavily rely on electronic equipment.

Regardless of whether you own or rent this equipment, it is crucial to carefully consider obtaining an electronic devices insurance policy that provides coverage for potential damages or replacement costs in the event of any unexpected accidents.

Counsellors we insure

Suited offers comprehensive insurance policies that cater to the needs of a wide range of counsellors, including:

- Student counsellors

- Career counsellors

- Mental health counsellors

- Rehabilitation counsellors

- Child counsellors

- Crisis counsellors

- Couples counsellors

- Trauma counsellors

- Grief counsellors

- Eating disorder counsellors

- Spiritual counsellors

- and more..

Shopping for counsellor liability insurance

Finding the right insurance for counsellors can be difficult. So, it's helpful to remember the following tips, no matter which insurance provider you decide to go with:

Cheap counsellor insurance

Don't just focus on finding cheap counsellor insurance - consider the quality of after-sales service too. Make sure you can easily reach your insurance provider when you need to. At Suited, we provide multiple contact options and ensure a prompt response.

The reputation of the insurer is important

Having reliable insurance is crucial for those moments when you require it the most. At Suited, we only work with financially stable insurers who hold an A+ rating, ensuring that you receive a payout when you need it.

Many providers charge fees to amend or cancel

Many insurance companies offer low initial prices, but this could be a tactic to conceal additional fees for monthly payments, policy amendments, or cancellations. We at Suited do not charge any other fees, and you can cancel your policy at any time without incurring any additional costs.

Some policy wordings are restrictive or have a high excess

While some insurance providers may offer attractive prices, they may compromise on the coverage provided. Suited's professional indemnity and public liability policies come with a £0 excess, ensuring that you receive the full coverage you need.

Common questions

Is professional indemnity insurance compulsory for counsellors?

Counsellors are not required by law to have a PI cover in place.

Will the work of my employees be covered by Suited therapists & counsellors insurance?

Yes, any work by bonafide employees of your business is covered.

What is the difference between therapy and counselling insurance?

From the insurance point of view these professions are very similar. With Suited you can include both of these professions in your PI and PL cover.

How is the cost of professional indemnity insurance for counsellors and therapists calculated?

At Suited we only take into account your annual turnover, that's it. We do not charge per person. PL cover cost is based on the limit you select.

CEO of Suited, with 20 years’ experience in business insurance, focused on building flexible, digital insurance solutions for SMEs and self-employed professionals.

Co-founder of Suited and insurance technology specialist, highly experienced in designing and delivering digital insurance solutions for SMEs and the self-employed.

Note

This guide is for informational purposes only and does not constitute advice or a personal recommendation.