What is insurance for copywriters?

Insurance for copywriters isn’t a single product. It consists of several products that combine to meet the specific insurance needs of a copywriter. The key product is professional indemnity insurance, which offers financial protection in situations where clients allege errors, omissions, or issues with the content produced. Other useful insurance covers can protect copywriters from unpaid invoices or assist with damaged work equipment.

Why do copywriters need insurance?

Copywriters produce content for clients’ briefs; however, the directions are interpreted by a copywriter in their own way. The creative direction can sometimes cause problems.

Protection from copyright infringement claims

Copywriters often work with various types of content, including images, slogans, or brand names. If a copywriter unintentionally uses copyrighted material without proper authorisation, it can lead to copyright infringement claims.

Mitigating defamation claims

Copywriters create content that promotes products, services, or ideas. Sometimes, the language used in advertising or marketing materials may be interpreted as defamatory by individuals or companies, leading to defamation claims.

Errors in professional advice

If as a copywriter you suggest a marketing strategy that does not yield the expected return on investment, insurance can cover the legal costs involved in defending against such a claim.

Content accuracy and misrepresentation

In the fast-paced world of copywriting, errors or misrepresentations in content can occur. If a copywriter unintentionally includes incorrect information or overstates the benefits of a product or service, it can lead to legal disputes.

For example, a copywriter might create promotional materials for a dietary supplement, inadvertently exaggerating its health benefits. Insurance can help cover legal expenses in such cases.

Professional indemnity insurance for copywriters

Professional indemnity insurance is a key cover that protects copywriters from accusations of professional mistakes, negligence, copyright infringement and other claims against you or your business.

It can help to legally shield from the specific risks that copywriters face in their profession and as such protect their career and financial well-being.

What does professional indemnity insurance for copywriters cover?

Professional indemnity insurance protects copywriters from claims or accusations of wrongdoing from their professional advice or work product.

Cover includes:

- Making a mistake

- Acting negligently

- Giving the wrong advice or recommendation

For example, you may be facing financial demands from a client because:

- You have included an image that you believed to be royalty-free, but it turns out to be copyrighted.

- you have drafted a product description that unintentionally damages a competitor's reputation.

- Your work closely resembles someone else’s content, and they’re asking for compensation.

- Your work caused offence and as a consequence, damaged your client’s reputation.

What professional indemnity limit do copywriters need?

When choosing a limit, consider several factors, including the value of your client contracts, your contractual requirements and obligations, and possible financial impacts if your content should cause an issue.

Does professional indemnity insurance cover my copywriting activities worldwide?

Worldwide cover depends on the provisions in your particular insurance policy. When checking your professional indemnity insurance documentation, always look for the ‘territory or geographical limits’ and ‘jurisdiction’ sections.

Territory or geographical limits:

The territory or geographical limits section tells you where in the world you can provide services. This refers to the virtual and physical delivery of your services.

Jurisdictional limit:

The jurisdictional limit specifies in which jurisdictions your policy will provide legal protection if you are sued.

As a service provider based in the UK, your best option is to sign contracts governed by UK jurisdiction. This dramatically reduces the risk of being sued outside your own country or in a jurisdiction that your policy may exclude.

What does Suited cover?

Suited professional indemnity covers your work anywhere in the world but will not cover claims brought against you in the US or Canada. Therefore if you work with clients in the US or Canada, do not enter contracts governed by those jurisdictions.

Switching your professional indemnity insurance

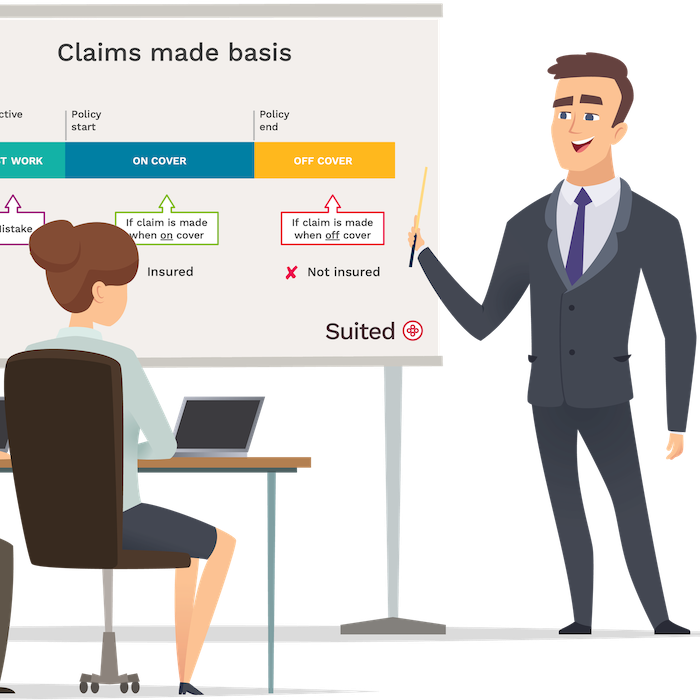

In the UK, most professional indemnity insurance works on a “claims-made basis”; this essentially means two things:

- You must have an active policy at the time a claim is made; and

- The policy period on your active policy must cover the time when the work was performed

When you cancel your professional indemnity policy, you can no longer make claims against that policy.

If you change provider, ensure your past work is covered, called “retroactive cover”.

Should I keep professional indemnity insurance if I pause or retire from self-employed copywriting?

It’s wise to keep your professional indemnity if you stop working as a freelance copywriter. Claims against professional misconduct can surface months or years after you delivered the work.

If a past client sues you for damages and you have cancelled your professional indemnity, you will not be covered.

How long you keep your cover in place is up to you; consider the type of work you did and the likelihood that a client might bring a claim against you.

Other useful insurance for copywriters

Other insurance copywriters might need will depend on your circumstances:

- Could you afford a legal dispute?

- Do you rely on expensive computer equipment for your income?

- How would you cover your business running costs if you fell ill?

- Do you have employees?

Commercial legal expenses

Commercial legal expenses insurance protects you and your business against commercial disputes, claims, criminal prosecutions, etc. It picks up various risks not covered by professional indemnity or public liability. This type of cover can provide access to advice, representation, and practical support when facing legal or regulatory challenges in the course of running your business.

Typical areas covered include:

- Legal and accountancy matters relating to your business

- Defence against criminal prosecution

- Compliance and regulatory investigations

- Pursuit of unpaid invoices (typically over a set threshold)

Examples of when it might be useful:

- Contract disputes

- You need to chase a client for a large unpaid invoice

- You’re facing a compliance issue and require expert legal guidance

Commercial legal expenses insurance often comes with access to helplines and resources to help navigate these situations more effectively.

Portable electronics insurance

More than ever copywriters rely on electronic equipment to deliver their services. If you depend on electronic equipment, consider electronic devices insurance to help you with covering replacement or repair costs.

Shopping for copywriters' insurance

Whether or not you decide to use Suited insurance for copywriters to protect yourself, it’s worth keeping the following in mind:

Price isn’t everything

Some providers offer rock-bottom prices, but after-sales service could be lacklustre. Check how easy it is to get in contact with your insurance provider. At Suited, we offer several options and answer quickly.

The reputation of the insurer is important

Insurance needs to be there when you need it most. The payout reputation of an insurer is essential. Suited uses financially sound insurers with an A+ rating.

Many providers charge fees to amend or cancel

Low initial prices often hide additional charges to pay monthly, amend or cancel your policy. At Suited, we charge no extra fees, and you can cancel anytime with no more to pay.

Some policy wordings are restrictive or have a high excess

Some providers will offer attractive prices, but it is at the expense of cover given. Suited professional indemnity and public liability have £0 excess.

Common questions

Do I need experience or qualifications to get insurance for my copywriting activities?

As a general rule, and it is certainly a condition with Suited, you must be able to demonstrate that you have relevant experience and/or qualifications to do your job.

I have only just completed my copywriting course. Can I get insurance?

Yes, if your course is relevant and recognised, you can get insurance with Suited.

Do copywriters need public liability insurance?

Only if you work with the members of the public or in public spaces or meet your clients face to face.

If I subcontract some work, will it be covered by Suited copywriting insurance?

Yes, but always check that your subcontractors are appropriately insured and never waive your rights to sue them for their mistakes.

CEO of Suited, with 20 years’ experience in business insurance, focused on building flexible, digital insurance solutions for SMEs and self-employed professionals.

Co-founder of Suited and insurance technology specialist, highly experienced in designing and delivering digital insurance solutions for SMEs and the self-employed.

Note

This guide is for informational purposes only and does not constitute advice or a personal recommendation.