What is business consultant insurance?

Business consultant insurance is not a single policy but rather a combination of insurance covers.

The first essential cover business consultants should seek is professional indemnity insurance. However, other covers may be required depending on your expertise and work methods. For instance, public liability insurance could be helpful if you engage with clients face-to-face or in public areas. Additionally, portable electronics insurance can help cover repairing or replacing your work gadgets.

Why do business consultants need insurance?

Stay compliant with a contract

As a business consultant, it is important to note that many contracts will require you to have professional indemnity insurance and provide proof of it. This requirement may still apply even after the completion of your contract.

IR35 enquiries

If you are contracting through your own limited company, it is possible that you may be subject to IR35 inquiries from HMRC.

Unpaid invoices and contract disputes

Independent business consultants may encounter problems with unpaid invoices and contract-related issues.

Accusation of causing a financial loss

Clients often seek your advice to resolve a business problem, but it is important to be aware that there is a possibility of being blamed for any financial harm caused by your recommendations.

Professional indemnity insurance for business consultants

Professional indemnity insurance protects business consultants against claims of negligence or inadequate advice that could lead to financial losses for your clients.

As a business consultant, it is important to be adaptable and provide innovative solutions to meet the ever-evolving needs of your clients. Despite your best efforts, there may be times when projects yield different results, which can lead to strained relationships and even legal disputes over compensation. Additionally, defending your reputation can be a time-consuming and costly process.

Therefore, it is crucial to have professional indemnity insurance to protect yourself and your business.

What does professional indemnity insurance for business consultants cover?

Business consultants can safeguard themselves from allegations of misconduct related to their professional advice or work product by acquiring professional indemnity insurance.

Cover includes:

- Failing your duty of care

- Acting negligently

- Giving the wrong advice or recommendation

- Confidentiality breaches

For example:

- A customer has expressed concern that the advice provided may have contributed to decreased sales.

- The suggestions made by you have resulted in a significant drop in productivity.

- The approach recommended did not produce the desired outcomes.

- Regrettably, confidential information regarding a client was mistakenly disclosed.

Does professional indemnity insurance cover my business activities worldwide?

If you work with clients outside the UK, you should check your policy for a couple of provisions. One is called ‘territory or geographical limits’ and the other ‘jurisdiction’.

Territory or geographical limits define where your work is covered. Whereas jurisdictional limit will define where you have legal protection against being sued by your clients.

For example, suppose your policy states a territory limit “worldwide” and a jurisdiction limit "worldwide excluding USA and Canada". It means that you can do work for clients based in the US and Canada but you won’t be insured for any claims brought up against you in those countries. However, if a US client tried to sue you in a UK court, your policy would respond.

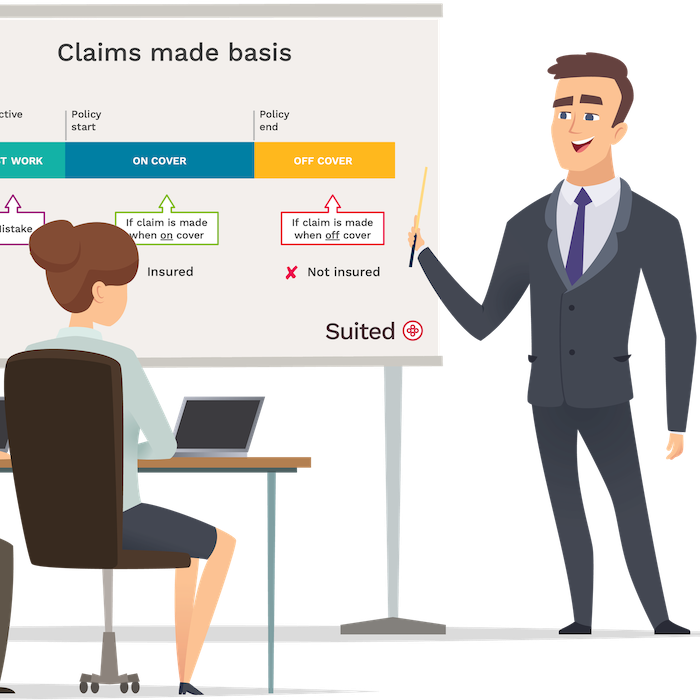

Switching or cancelling professional indemnity insurance for business consultants

If you cancel your professional indemnity policy in the UK, you cannot make any claims against it.

Therefore, when switching to a new business consultant insurance provider, it is important to ensure that your new policy includes coverage for your previous work, referred to as "retroactive cover".

Should I keep professional indemnity insurance if I take a break from business consulting?

It’s wise to keep your professional indemnity if you retire or take a break from business consulting. Claims against professional misconduct can surface months or years after you delivered the work.

If a past client sues you for damages and you have cancelled your professional indemnity, you will not be covered.

How long you keep your cover in place is up to you; consider the type of consulting you did and the likelihood that a client might bring a claim against you.

Public liability insurance for business consultants

Public liability insurance shields business consultants from claims of injuries or property damage.

If you interact with clients or the public in person for your business, there is a chance of causing injury or damage to their property. Even a minor accident, like spilling your coffee on a client's laptop, can result in significant financial loss.

Public liability insurance offers affordable coverage for unexpected incidents such as slips, falls, or accidental damage to someone else's equipment. It protects third-party claims and safeguards your business from potential lawsuits.

What does business consultant public liability insurance cover?

Having public liability insurance can be very helpful in the event of injury claims and demands for compensation.

Cover includes:

- accidental injury or death

- accidental property damage

For example:

- A client, while visiting your place of work, suffered s trip. Some days later, you’re asked by their solicitor to pay the medical costs and compensation.

- You bought your client a hot drink. They picked it up but dropped it, spilling the hot liquid all over their pricey possessions or clothing. You may not think it was your fault but your client may seek compensation.

Other insurance for business consultants buy

Commercial legal expenses

Commercial legal expenses insurance is designed to support professionals such as counsellors with a range of legal and tax-related matters that fall outside the scope of professional indemnity or public liability insurance.

This type of cover can provide access to advice, representation, and practical support when facing legal or regulatory challenges in the course of running your business.

Typical areas covered include:

- Legal and accountancy matters relating to your business

- Defence against criminal prosecution

- Compliance and regulatory investigations

- Pursuit of unpaid invoices (typically over a set threshold)

Examples of when it might be useful:

- Contractual disputes

- You need to chase a client for a large unpaid invoice

- You’re facing a compliance issue and require expert legal guidance

Commercial legal expenses insurance often comes with access to helplines and resources to help navigate these situations more effectively.

Portable electronics insurance

If you work as a business consultant, you probably rely on various gadgets and equipment to perform your job. If the cost of this equipment is high, it would be prudent to have portable electronics insurance.

This insurance can assist with the expenses of repairing or replacing your work belongings in case they are stolen or unintentionally damaged.

Shopping for business consultant insurance

If you're considering using Suited for your business consultant insurance, it's important to keep the following factors in mind:

Cheap business consultant insurance

While some providers may offer very low prices, they may not offer great after-sales service or have expertise in your specific industry. At Suited, we offer multiple ways to contact us and provide quick responses.

Check the insurer's reputation

Ultimately, insurance needs to be there when you need it most. That's why Suited only uses financially sound insurers with a top A+ rating for payout reputation.

Look for run-off and retroactive cover options

Some insurance providers don't offer cover for past incidents or the ability to switch your professional indemnity to a run-off mode. But at Suited, we offer both.

Watch out for restrictive policy wordings or high excess

Some providers may offer attractive prices but limit the coverage they provide. Suited's professional indemnity and public liability policies have a £0 excess.

Common questions

What does consultant business insurance do?

Business consultant insurance protects against legal claims, equipment loss, and health risks. Finding the right insurance mix that reflects your business operations and risk tolerance is essential.

Do self-employed business consultants need insurance?

For self-employed business consultants, having business insurance is essential. It safeguards your finances and can shield your reputation in the industry. With the uncertainties and risks associated with running an independent consultancy, insurance coverage is a prudent choice to ensure you stay protected and can continue to operate with peace of mind.

Do business consultants require employers’ liability insurance?

Business consultants are not obliged to obtain employer's liability insurance when they operate independently. However, you will likely need it if you engage volunteers or sub-contractors in your operations. It's your responsibility to ensure that you are aware of and comply with all legal requirements and obligations.

When do business consultants need insurance?

As an independent business consultant, having the appropriate insurance when working on a contract or operating independently is crucial. The required insurance will often be outlined in your contract with the client. However, even if it is not required, it is wise to consider obtaining business insurance in the event any unexpected issues happen with your work or business relationships.

CEO of Suited, with 20 years’ experience in business insurance, focused on building flexible, digital insurance solutions for SMEs and self-employed professionals.

Co-founder of Suited and insurance technology specialist, highly experienced in designing and delivering digital insurance solutions for SMEs and the self-employed.

Note

This guide is for informational purposes only and does not constitute advice or a personal recommendation.